WEALTH CREATION THROUGH MUTUAL FUNDS

Building Wealth From Salary: A Dual-Scenario Retirement Strategy for Rohan

Client Profile & Assumptions

Name: Rohan Mehta

Current Age: 32 years

Retirement Age: 60 years (Investment horizon of 28 years)

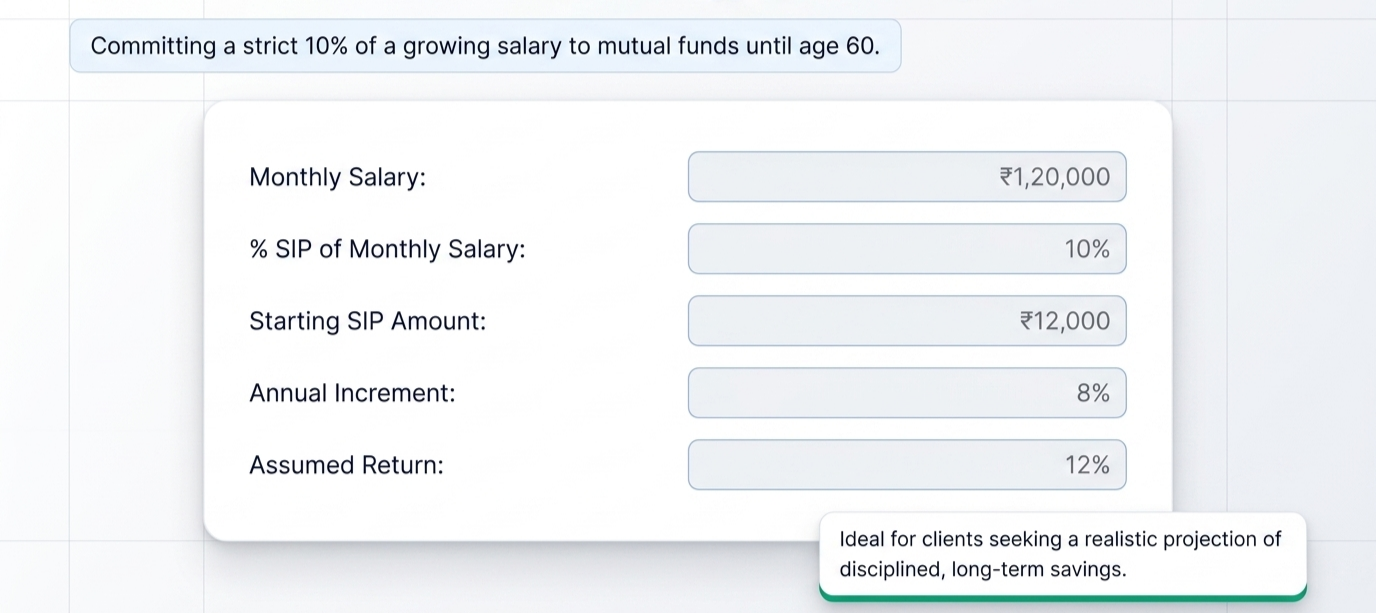

Starting Monthly Salary: ₹1,20,000 with an expected 8% annual increment

Existing Equity Mutual Fund Portfolio: ₹6,00,000

Assumed Rate of Return: 12% p.a. on both new SIPs and existing investments

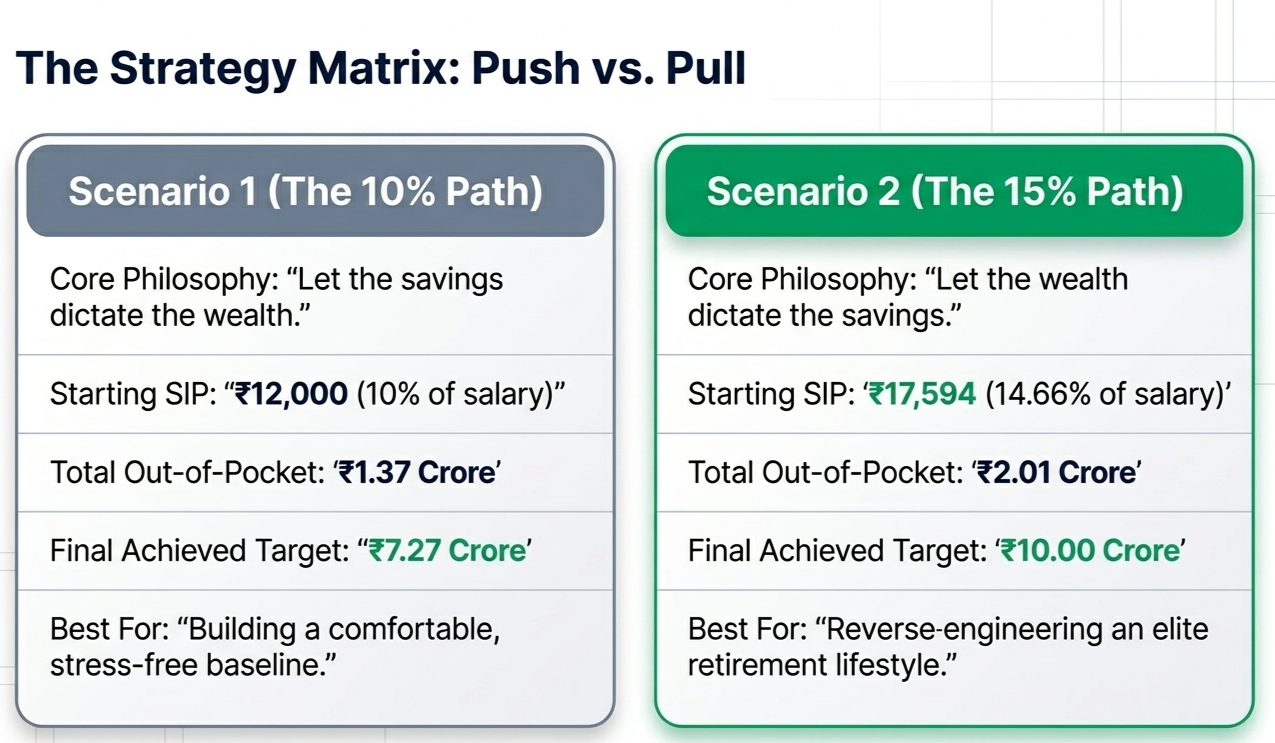

Scenario 1: Wealth Creation via a Fixed % of Salary

This scenario projects the total wealth Rohan can accumulate if he starts by investing 10% of his current monthly salary (₹12,000/month) as a Systematic Investment Plan (SIP), increasing his investment amount by 8% every year in line with his salary increments.

The Numbers:

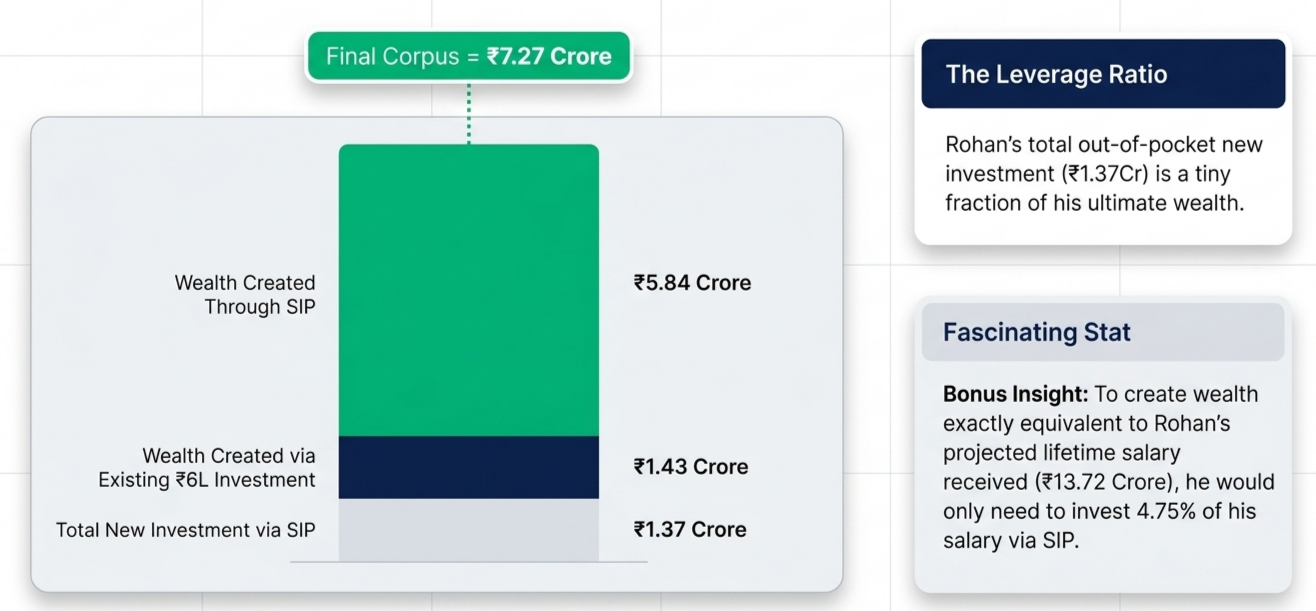

Total Salary Received (over 28 years): ₹13,72,87,915

Total New Investment via SIP: ₹1,37,28,791

Wealth Created via SIP: ₹5,84,32,619

Growth of Existing Investment: ₹1,43,30,320

Total Projected Retirement Corpus:₹7,27,62,939

Key Insight: By simply allocating 10% of his growing income, Rohan’s total retirement corpus can reach over ₹7.27 crore. The step-up feature (linking SIPs to annual salary raises) drastically maximizes his wealth creation without straining his current lifestyle.

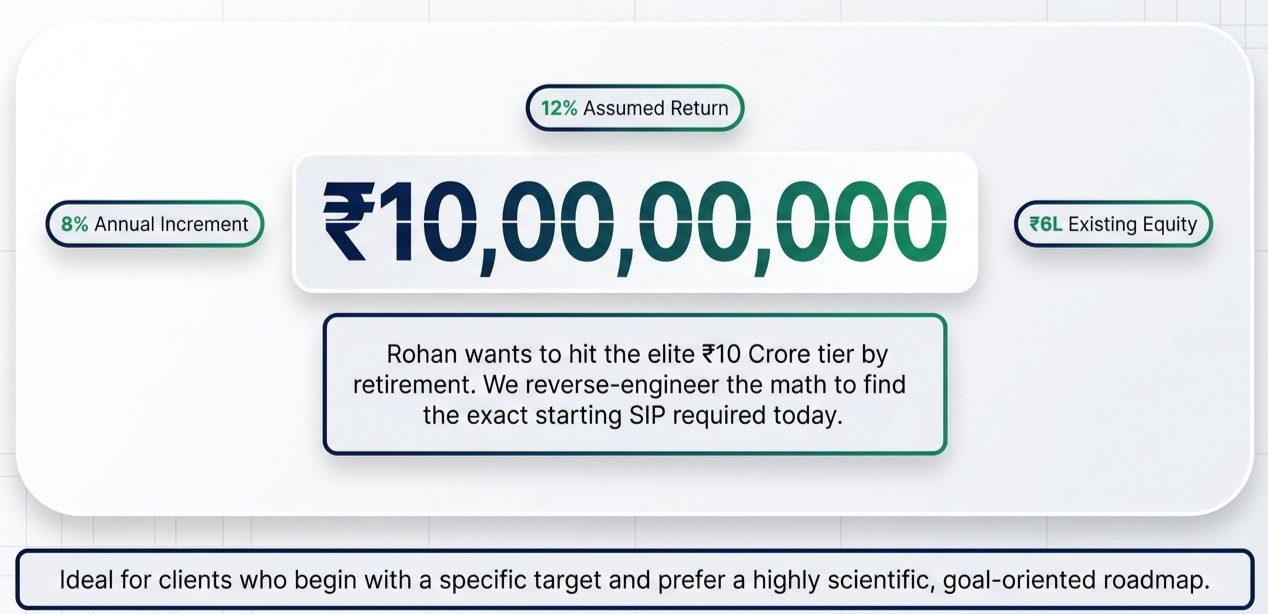

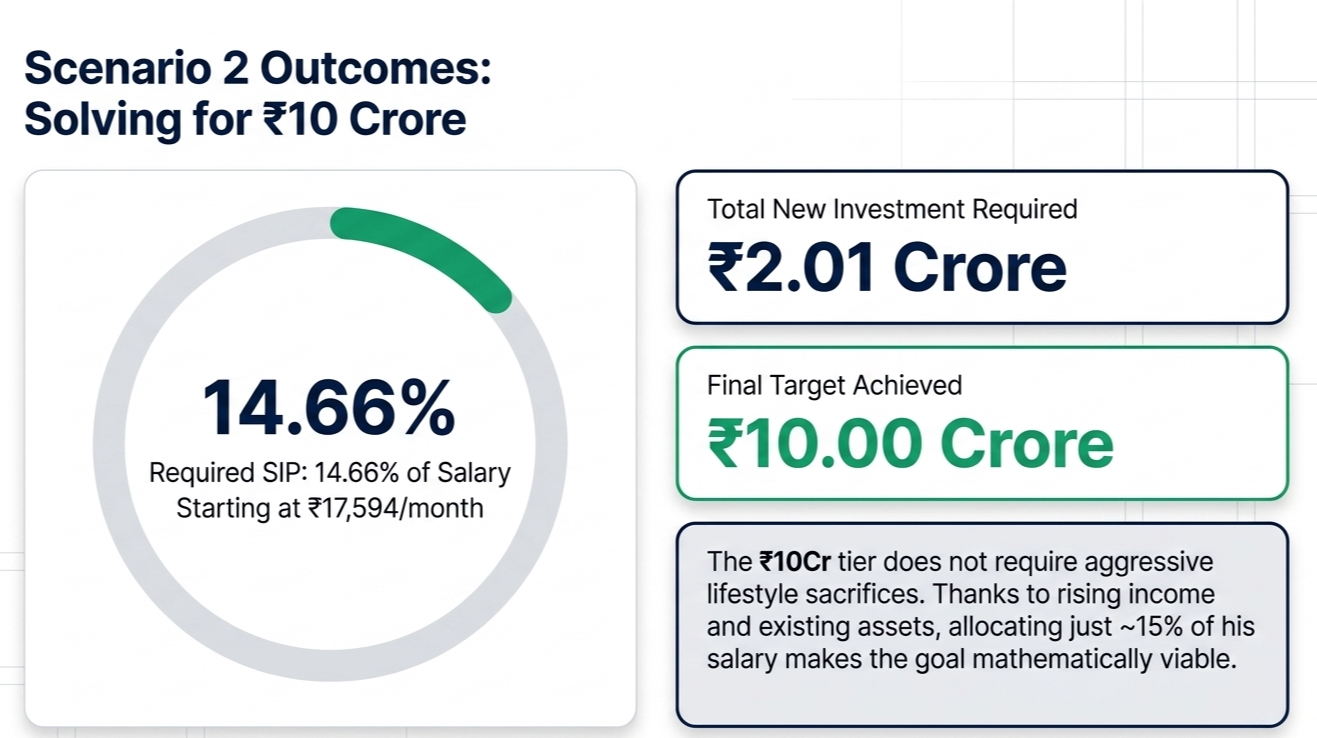

Scenario 2: Savings Required for a Target Corpus

While Rohan’s initial thought was a ₹5 crore target , this calculation evaluates what is required to hit a more ambitious target retirement corpus of ₹10,00,00,000 (₹10 Crore).

The Numbers:

Starting Monthly SIP Required: ₹17,594

Required Savings Rate:14.66% of his current salary

Total New Investment Till Age 60: ₹2,01,28,161

Key Insight: Rohan does not need to invest aggressively to hit the ₹10 crore mark. Because compounding does the heavy lifting on both his existing ₹6 lakh portfolio and his step-up SIPs, a starting investment of roughly 15% of his salary is completely sufficient.

Final Roadmap & Recommendation

Rohan is in an incredibly strong position to secure a comfortable retirement. The definitive recommendation to move forward is:

Aim for the 15% Mark: Instead of starting at 10% (which yields ₹7.2 crore) , Rohan should optimally start his monthly SIP at ₹17,594 (approx. 15% of his current salary).

Automate the Step-Up: He must ensure his mutual fund SIPs are set to automatically increase by 8% every year. This ensures that as his salary grows, his wealth accumulation effortlessly stays ahead of inflation.

Leave Existing Assets Untouched: The existing ₹6 lakh equity portfolio is projected to grow to over ₹1.43 crore on its own. Keeping this bucket strictly cordoned off for retirement is vital to achieving these final milestones.

To know more, feel free to contact us.

From Our Investors

-

![Testimonials]()

AN AMAZING GENTLEMAN WHO PLANS YOUR INVESTMENTS FOR YOUR BRIGHT FUTURE.... PLEASE DO PAY A VISIT AND IF YOU ARE CONVINCED, I AM SURE OF WHICH YOU WILL BE ... YOU WILL AUTOMATICALLY WILL INVEST

Colonel Puneet Khanna

-

![Testimonials]()

A great help for investors. It is the best platform where everyone is free to clear their doubts regarding investment.

Dr. DURGESH AGNIHOTRI , Associate Professor - PSIT Kanpur

-

![Testimonials]()

I approached Hari by recommendation of one of my friend because I asked for an independent advisor not employed by a bank and not committed to sell the bank’s financial product. I read articles in Financial Kundali and they were real eye opener. Products which I thought can be investment are actually not. Hari is a BRILLIANT financial planner and he has all of the best qualities of a professional adviser.

SHIVANGI GUPTA

UniSuper Automation Test Consultant,

MELBOURNE, AUSTRALIA

-

![Testimonials]()

Earlier, Financial Planning was like a nightmare for me. But Hari’s insightful advice went a long way in changing my outlook towards money and helping me achieve my financial goals. I would really recommend Hari as an experienced financial consultant to help you with planning your portfolio and achieving financial freedom!

RAAHUL SINGH GAUTAM,

Capgemini Senior Consultant, Mumbai

-

![Testimonials]()

Description goes hereI am one of the those very few people who attached with Financial Kundali in its Starting stage. Mr Hariom Tripathi ji is very nice person and he is having good knowledge.

DINESH SINGH CHAUHAN,

Balrampur Chini Mill

-

![Testimonials]()

Phenomenal website. Boon for guys like me who are challenged with Financial Quotient. Articles are as easy as pie, limpid, lucid & articulative. Besides, enough fodder is available for intellectual nourishment. I was personally impressed by an analytic and interpretive article which compares PPF & LIC as tax-saving investments.

GAURAV TRIPATHI,

Manager, Indian Overseas Bank, LUCKNOW

-

![Testimonials]()

Great experience. They have in depth understanding and are able to align the financial goals with investments. Above all, they are passionate about their work. Highly recommended!!

SHRIDHAR RATHORE, TCS, USA

-

![Testimonials]()

It was a nightmare when while my Financial Planning Discussions. Hari Om analyzed on how i was investing in my insurance policy for 21 years and getting a very nominal return. With his guidance I invested partially in Term Plan & Mutual Funds. Now I am fully insured & expecting a 40-50% more return from my last policy & guess what my money is not blocked for decades for God sake. Hari trust me this is a charity you are doing to World. Thanks for saving my Money. All the very best.

GAURAV TRIPATHI,

Godrej & Boyce Mfg Co. Ltd., Manager Storage Solutions, New Delhi

-

![Testimonials]()

I am absolutely delighted with your service. It's really refreshing to work with a financial adviser who is truly interested in their client's needs, circumstances and preferences. What really impressed me was the way you took the time to get a feeling for where i was at, your depth of knowledge, lateral thinking and your common-sense approach. Your professional, ethical and caring demeanour elicits my trust and respect and I gladly recommend your services whenever possible.

RONAK TANDON, FUTURE TRUCKS KANPUR

-

![Testimonials]()

A very good initiative has been taken by Mr. Hari Om Tripathi to work on this way. This site is a very effective tool to cross check all your financial myths. As a layman people generally find it difficult to get the right product as per their financial need or goal. This site is making them self-enabled to judge the right product. It is covering almost all the financial products and giving insight on that. Overall, a great financial site that i recommend.

DEEPIKA SINGH

Axis Bank, Deputy Manager, New Delhi

-

![Testimonials]()

A Way to start your Financial Life While searching for some financial planning related websites, I came across this website. I liked the site very much. It provides all the basic information for common people to improve their financial Life. It has very good services like Free Financial Health Check list, Goal Based Investment, How to manage your Financial Wealth etc. All the topics are discussed in a nice way. As a newcomer to making financial decisions I have needed all that I could get. Hari Om has always shown great patience and explained things clearly and thoroughly without being patronising. He always respected my wishes with regard to risk taking and made me feel comfortable with the decisions I have made.

MAHESH MAHATEKAR,

Xecom IT Pvt. Ltd., Lead QA, Pune